When compared with peers, fund managers consistently argue that their investment team is best positioned for outperformance given their various characteristics. Given that we encounter investment teams that come in all shapes and sizes, this insights piece seeks to quantify the optimal characteristics of an investment team, based on the performance of our rated managers.

How have investment teams changed in recent years?

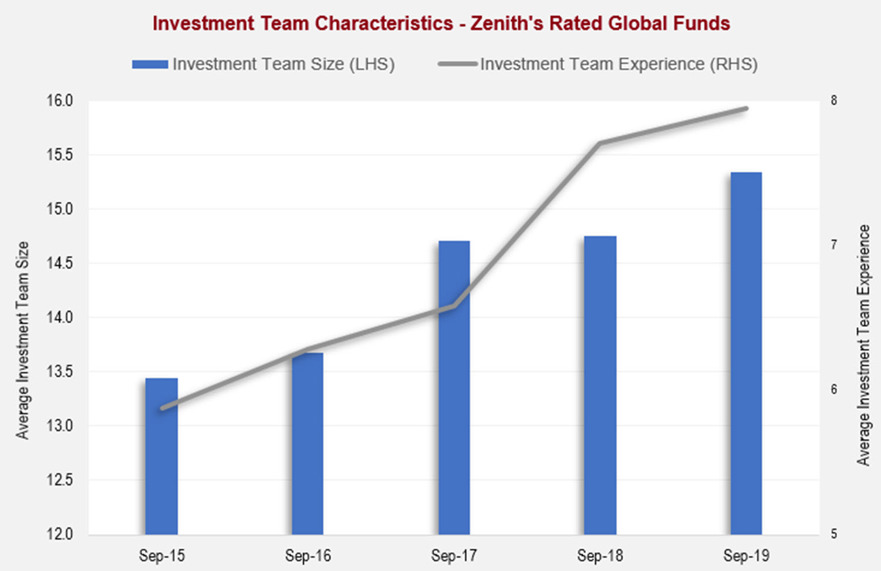

With the second Markets in Financial Instruments Directive (MiFID II) directly causing highly sought-after talent to move from the sell-side to the buy-side, fund managers (buy-side) have been the ultimate beneficiaries. This effect can be measured through the headcount amongst fund managers and the corresponding levels of investment team experience, as shown in the chart below.

We found that the average team size has increased every year since 2015, with the most significant increase occurring over 2018 when MiFID II was enforced. In addition, the new hires did not detract from the overall team experience, which indicates that managers were able to add experienced individuals.

Is bigger necessarily better?

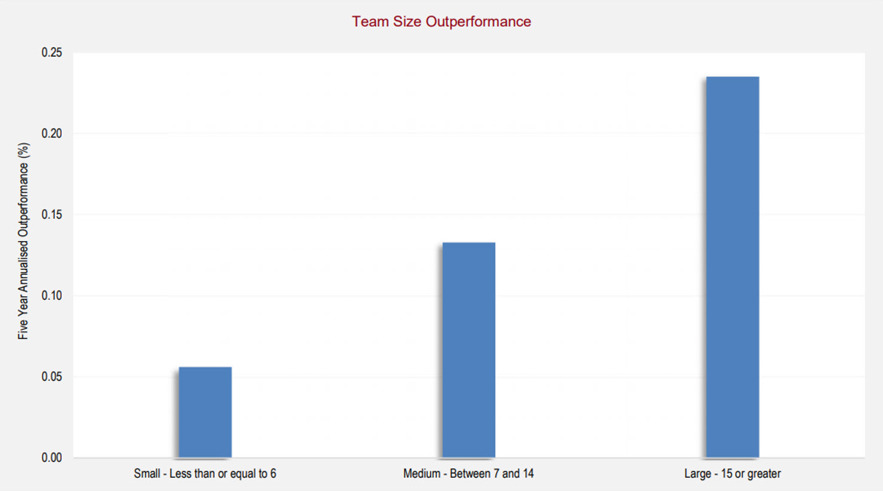

To answer this question, we performed an analysis of the fundamentally-driven global equities managers on Zenith’s approved product list over the five years to 30 September 2019. As part of the study, we grouped the size of the investment teams into three equal categories – small (less than or equal to 6), medium (between 7 and 14) and large (15 or greater).

The results of the study are shown in the chart below.

The chart suggests a positive relationship exists between the size of the team and outperformance, meaning larger teams tend to experience greater levels of outperformance on average as compared to smaller teams.

Do too many cooks spoil the broth?

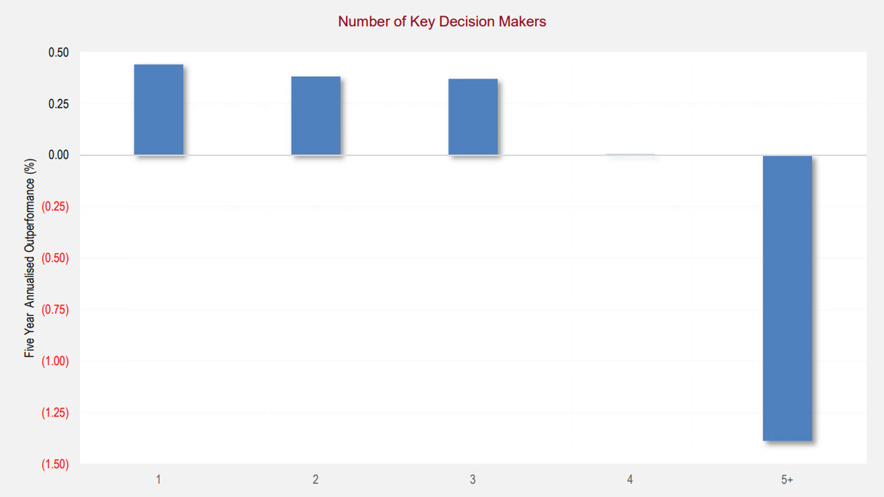

Managers that adopt a more compact decision-making approach would argue that they benefit from greater levels of accountability and nimbleness. However, managers that adopt an investment committee approach believe that they are better able to share investment insights and experience.

The chart below shows the performance of managers based on the number of portfolio managers or key decision-makers.

The numbers suggest that the fewer key decision-makers in an investment team, the greater the level of outperformance. However, we note that the performance of the five and above category may not be a true reflection of the overall population, given our small sample size for the group.

Have we found the magic formula?

Our study suggests that large teams driven by a compact decision-making approach tend to exhibit greater levels of outperformance compared to alternative structures. Yet, ultimately, we do not believe there is a single template that managers should follow to succeed. We have reviewed successful managers that do not align with the above and unsuccessful ones that mirror the ideal template.

Overall, a team’s ideal structure needs to align with its investment philosophy and process.