Key points

- Secular trends are disrupting the retail, office and industrial sectors. But these trends are also supporting the emergence of alternative sectors.

- Alternative real estate can be less cyclical and less correlated to core real estate markets as they are driven by different secular and structural themes.

- Themes driving alternative real estate include demographic, social and technological forces as well as investors increasingly seeking to add diversification around core sectors.

- A growing opportunity set in alternative real estate, much of which is less sensitive to the direct impact of the pandemic, is creating additional opportunities for investors.

As difficult as it is to envisage, there is life beyond COVID-19 for real estate.

While performance of Australian Real Estate Investment Trusts (A-REITs) has been challenging, it is not unexpected given the rapid implementation of the global shutdown and isolation measures. Property’s performance is fundamentally underpinned by activity and interaction between people. Accordingly, social distancing policies enacted around the world have had a profound impact on the usage of commercial property.

With A-REITs being traditionally highly concentrated in retail, office and industrial, secular trends are disrupting these sectors to varying degrees. These trends are also supporting the emergence of alternative sectors of the market and expanding the frontiers of A-REITs.

Alternative real estate – what’s in a name?

There is no firm definition of what makes up ‘alternatives’ in real estate, although it can generally be used to encompass sectors outside the core sectors of office, retail and industrial. This includes more established sectors such as hotels and healthcare, emerging sectors such as student accommodation and self-storage and developing sectors such as data centres. Investors are attracted to alternative sectors as they can provide diversification to REIT portfolios with differing levels of cyclicality, structural secular tailwinds and longer lease profiles.

Investor interest in alternative real estate reflects a decade-long trend of strong capital markets which has resulted in intense competition for assets in core sectors. Investors are also recognising the long-term secular trends driving the sector and seeking to position themselves in those sectors that have structural tailwinds. Population centric issues such as overall growth, urban densification and aging are combining with housing affordability, globalisation and technology to reshape the market.

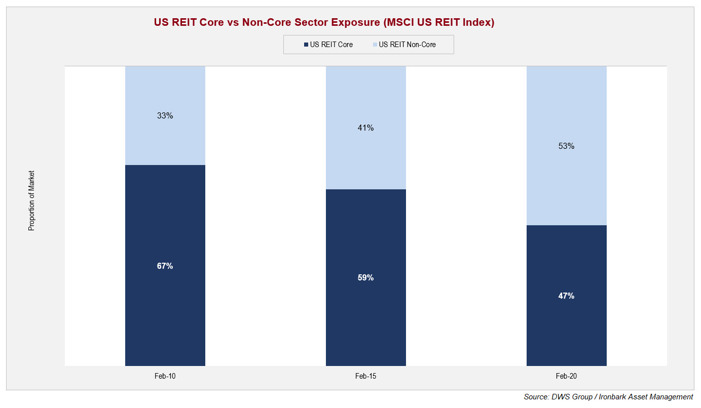

While the extent of alternative sectors remains small relative to core, the A-REIT market is following established trends offshore which are visible in Global Real Estate Investment Trusts (G-REITs), particularly the U.S. and the U.K. As an example, the shift in the U.S. is depicted in the following chart. While local markets remain comparatively small (approximately 6.5% of the S&P/ASX 300 AREIT Index comprises alternative segments as at 31 March 2020), we believe that this is an important trend indicator as markets evolve.

Notwithstanding the appeal of these alternative real estate sectors, they face challenges as well. Such markets are generally less developed, meaning there is less available market data, market depth (liquidity) and a restricted ability to achieve scale. They can also result in material operational business exposure, regulatory risk and greater exposure to supply shocks.

Within the A-REIT market many alternative real estate companies are smaller capitalisation securities which brings its own range of challenges. While some areas of the market will undoubtedly always remain highly niche, a broadening of the opportunity set for managers is likely to bring further rewards.

Alternative benefits

The increase in accessibility of alternative real estate is important for portfolio allocators as historically, the core sectors have a strong linkage to the economic cycle. Traditionally, the core sectors of office, retail (particularly discretionary) and industrial tend to be pro-cyclical and as such these returns carry a moderate to strong correlation to each other. Alternative real estate however can be less cyclical and less correlated to core real estate markets as they are driven by different secular and structural themes.

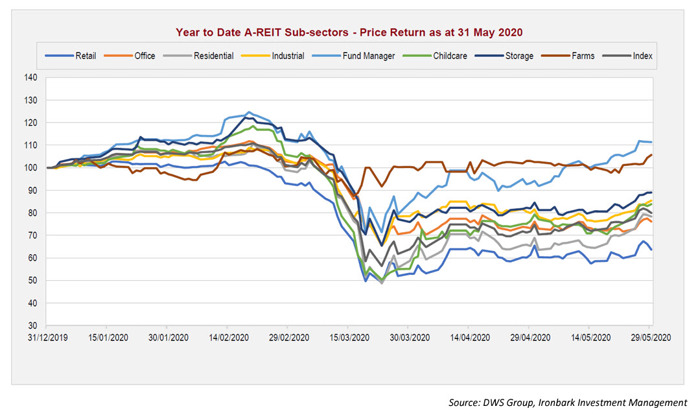

This can be clearly seen when decomposing the performance of the A-REIT market during the early stage of the pandemic. While overall the impact of COVID-19 has been severe, it has not been uniform, with different segments of the A-REIT market moving at varying speeds.

Expanding the themes

Aside from pure economic forces, themes driving the alternative real estate sector include demographic, social and technological forces. These structural trends also include longer-term capital market actions as investors seek to add diversification around the core segments.

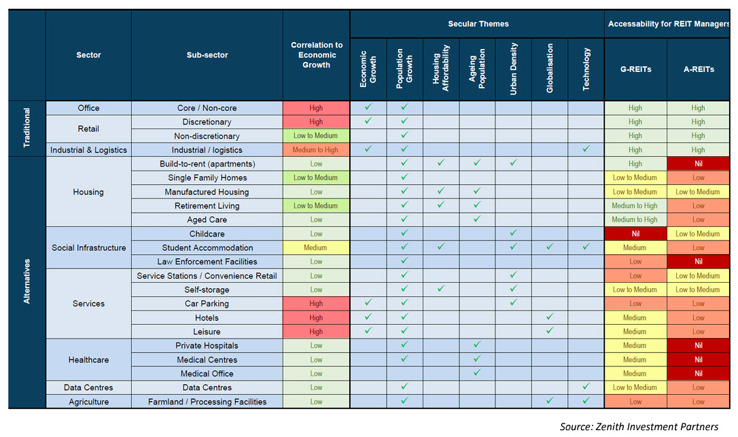

In the following table, we outline the major traditional and alternative real estate sectors in terms of their secular drivers and linkage to the economy. We have also sought to indicate the level of accessibility to investors within both A-REIT and G-REIT markets.

Alternative real estate also embraces a wide range of lease structures. In stabilised commercial real estate, the relationship between income and value is heavily influenced by:

- The length and quality of the cashflow,

- The risk of that cashflow being interrupted by a default,

- The probability of establishing a new cashflow and its pricing once the existing cashflow has expired or been terminated.

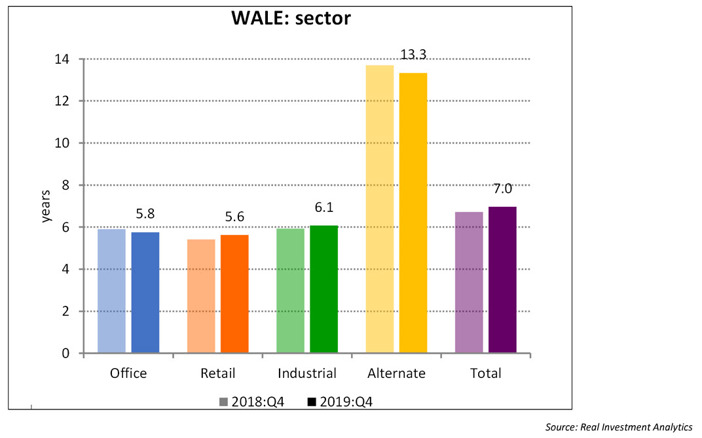

In periods of strong market growth, properties with a shorter Weighted Average Lease Expiry (WALE) are generally more able to capture reversionary upside on reletting. However, longer leases generally provide a level of protection during periods where markets are challenged as they are less exposed to the risks associated with negative rent reversions.

Many segments of the alternatives real estate market tend to have longer lease terms than the traditional sectors. This can be seen in the following chart which shows the aggregate WALE across the Australian commercial property market.

There are obvious benefits in having some exposure to alternative real estate sectors. Alternative sectors with their different drivers, can offer lower cyclicality, reducing REIT portfolio volatility and enhancing risk-adjusted returns. Furthermore, many alternative sectors are better positioned to capture long-term secular market themes than traditional property sectors. In addition to differentiated cyclical and secular drivers, the longer lease profiles of alternative sectors can provide additional diversification benefits to A-REIT portfolios.

The future is coming fast

What does the future hold for real estate in a post-COVID-19 world?

At this point, the short-to-medium term impact on real estate remains largely unclear. However, as with all periods of turmoil, demand for weaker assets across all segments will decline. COVID-19 has brought new uncertainties and there are likely to be substantial changes across different sub-sectors and an acceleration of structural changes across the industry.

Although the current situation remains highly fluid, COVID-19 is unlikely to radically transform demand for quality real estate in the long-term. While the world must learn to adjust to a new normal, quality assets should remain in strong demand. However, landlords need to move rapidly to accommodate both short-term necessities and longer-term trends to ensure assets remain resilient against economic fallout from the pandemic.

Following the path of offshore trends, we expect further growth in alternative real estate markets, driven by secular and structural trends which continue to gain momentum. An increasing opportunity set in alternative real estate segments, many of which are likely to be less sensitive to the direct impact of the pandemic, creates additional opportunities for investors.

While undoubtedly some areas of the market will always remain highly niche, a broadening of the opportunity set for managers is likely to bring further rewards. Ultimately, we believe that the rise of alternative real estate offers an investment thesis which is strongly complementary to more traditional real estate sectors. We continue to observe the sector closely as the rise of alternative real estate edges closer to the mainstream.