The intensifying focus on sustainability factors across investment markets has been a logical response to recent trends being driven by tenants, investors, asset owners and regulators. However, it should be remembered that the property industry has been embedding issues on sustainability for many years. Real estate portfolios comprise long-dated assets which not only have an outsized exposure to a range of risks across the Environmental, Social and Governance pillars, but are also material consumers of vital inputs such as energy. As such, leading asset owners in this space have long been proponents of implementing greater efficiencies for critical inputs as this has a meaningful impact on asset profitability as well as meeting increasingly robust sustainability agendas. In addition to the physical assets, property securities operate under comprehensive governance related considerations common with broader equities.

Energy efficiency has led the way…

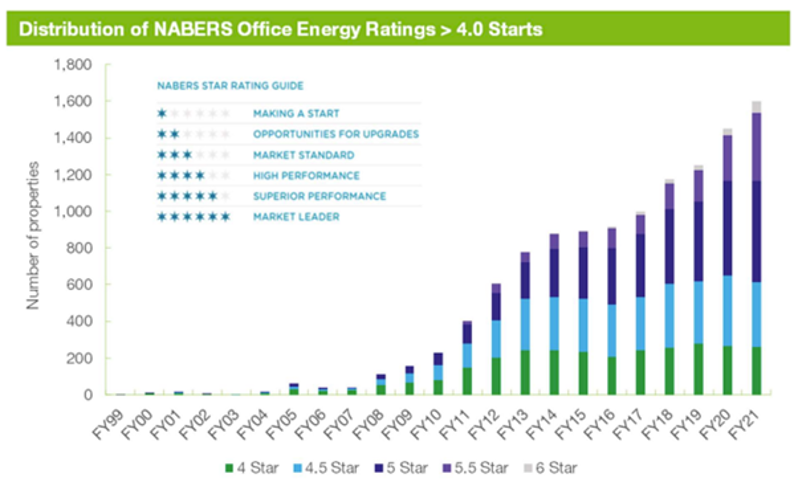

The Australian market has been at the forefront on legislating disclosure in the commercial real estate market across efficiency regarding energy, water and other indicators, an approach increasingly adopted by other countries. For example, the National Australian Built Environment Rating System (NABERS) is a key sustainability rating standard which provides an energy efficiency rating for buildings. It can be seen in the following chart, that not only has there been strong growth in ratings driven by regulation, but also a shift towards higher ratings.

Source: NABERS, Zenith Investment Partners

There are also indications of a “green premium” in real estate, where properties built to high energy standards command value and rent premiums. Indications in Australia, where mandatory energy ratings for most commercial assets have been in effect since 2010, have been notable, results show that high-rated properties generally had premiums on capital values, over low-rated properties.

New issues are arising

While key issues such as greater energy and water efficiency have been part of the sustainability agenda for many years, the rise of new considerations has been fast paced, as has the increased materiality of key topics for REITs. Key issues arising in the last five years include:

- Modern slavery issues (key examples include facilities cleaning and construction contractors)

- Carbon and carbon neutrality (including portfolio level targets)

- Resilience (against climate change risks i.e. extreme weather, rising water levels etc.)

- Interior environment (air quality, thermal comfort, lighting and acoustic control)

- Waste management (increased recycling efficiency)

The ‘green premium’ has long pointed to increased tenant demand, lower incentives, lower operational costs and ultimately higher net investment incomes and greater property values for more sustainable properties. However, we note that in addition, the above factors can impact cashflows through other avenues like higher capital expenditure costs over time and increased insurance costs/inability to insure. Furthermore, we note the increasing challenges from a measurement, reporting and regulatory perspective common among all asset managers and corporations.

The focus on carbon

The focus on carbon provides both opportunities and challenges for REIT investors, as decarbonisation pathways for real estate vary widely by both country and sector due to differences in government targets and building energy mix. Furthermore, there’s a wide dispersion in emission intensity within the energy networks across the major G-REIT markets as well across major sectors. As we move towards net zero and beyond, there’s a shift underway from thinking only about operational carbon to a ‘whole of life’ approach to account for emissions along the value chain. Simply put, ‘whole-life carbon’ must be split into two main sources:

- Embodied carbon - carbon emitted to construct, maintain, and demolish a building

- Operational carbon - emissions caused during the operation of a building e.g. energy used for heating, lighting, appliances, etc.

This creates several challenges. Embodied carbon is locked-in at the construction stage, and as such relies on a multi-front industry engagement to address issues across design, material and construction methods in order to reduce carbon emissions intensity.

Whose carbon is it?

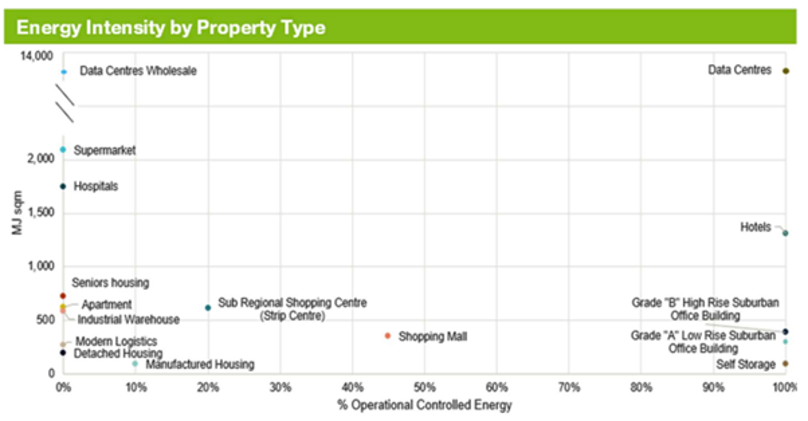

While operational carbon can be reduced over time through initiatives such as on-site power generation and shifting to renewable energy sources via procurement, additional challenges remain. Considerations of ‘controlled’ and ‘non-controlled’ operational carbon become a key consideration in REITs given the potential for lease and/or fund structures to create a barrier between the asset owner and operational emissions.

For example, a REIT reports on those operations where it controls operating policies. However, if tenants lease space under triple net leases or assets are held under a joint venture, influence over sustainability initiatives and performance may be limited. As an example, this can be seen in the following chart when viewing the energy intensity of the G-REIT universe through the lens of different levels of operational control.

Source: First Sentier Investors

How are managers responding?

We’ve observed through our Responsible Investment Classification frameworks, that managers investing in asset classes associated with the built environment (i.e., property and infrastructure), show a greater propensity to engage in high level of Environmental, Social and Governance (ESG) incorporation into investment analysis compared with general equities and other asset classes. We view this as logical given the longstanding focus of asset owners on a range of sustainability issues as discussed above.

For active managers in our peer group, company-level assessments of E, S and G issues are integral to stock selection. Depending on the approach, these can influence assessment of the impact on short and long-term cashflows, regulatory frameworks and management quality. These considerations are all incorporated differently across the peer group but typically influence valuations (cashflows and/or discount rates), quality metrics and ESG scores.

While early actors on decarbonisation issues have typically adopted active ownership strategies like company engagement and proxy voting to address issues at ground level, increasingly we see managers also utilising fundamental analysis as a way to model scenarios and engage in stress testing regarding company valuations. We expect these activities to increase as data availability and integrity increases.

Given the complexities involved for companies to navigate the transition to net zero, we highlight the importance of the allocation of capital by specialist REIT investors. While not discounting the role of index managers in undertaking company engagement, we also consider the transition to be particularly favourable environment for active management. From both a valuation and risk mitigation perspective there will be opportunities and threats as we continue to see society’s critical assets evolve and the underlying universe change. This is an area we will continue to watch as company and manager commitments to net zero initiatives evolve.