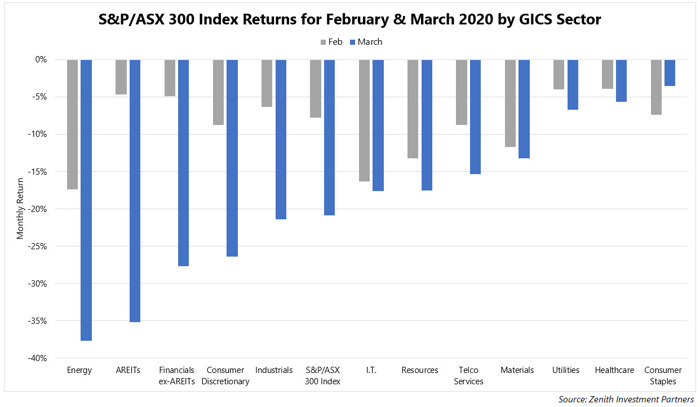

For investors in Australian Real Estate Investment Trusts (AREITs), March 2020 has been an unhappy month. While their defensive status held up well against the broader S&P/ASX 300 Index in February (as shown in the following chart), the following month saw the S&P/ASX 300 AREIT Index fall heavily, with a return of -35% as fears around the impact of COVID-19 hit home.

AREITs also fell materially more than their Global REIT (GREIT) counterparts in March, which saw the FTSE EPRA/NAREIT Developed $A (Hedged) Index deliver -23%. Much of the difference in relative performance was caused by the relatively higher exposure to the retail sector in the AREIT Index. This segment has been especially hard hit due to the dramatic decrease in foot traffic as isolation policies take hold.

By comparison, GREITs have greater exposure to property markets that have been less impacted by COVID-19, such as residential housing, healthcare and data centres. They also typically limit non-rental activities. This has meant that their overall performance has held up better in the face of uncertainty. In the face of the economic fallout of COVID-19, the performance of REITs in general and AREITs relative to GREITs is resulting in several key questions from investors, namely:

- Why maintain an exposure to listed property? Does this make sense given the outlook?

- Does it make sense to maintain exposure to AREITs relative to more diversified GREITs?

This is not 2008…

Where the last downturn was triggered by a global credit crisis, this is a public health crisis delivering an exogenous shock to the world economy.

During the GFC, any capital intensive industry that relied on meaningful levels of debt was hit hard and early, with REITs suffering some of the worst punishment.

In the wake of that experience, most REITs have subsequently been cautious with their balance sheets. Most are well positioned, with lower gearing, more diversified debt sources, longer debt tenure and higher interest coverage levels.

…but 2020 won’t be pretty either

Obviously, markets are whipsawing massively as they try to understand the ramifications of COVID-19. Real estate is no exception as the flow on impact of social isolation is proving very disruptive for tenants and how they carry on with their business. Property tends to fundamentally be an industry which brings people together to interact, so forcing them apart brings immediate operational dislocation.

Economies operate on the relationship between supply, demand and finance. The pandemic has caused a simultaneous shock to all three aspects, disrupting global supply chains, impacting consumption, shutting down business across both the manufacturing and service sectors and destabilising financial markets.

As tangible assets, property has generally performed well in times of market stress, providing diversification benefits and more stable income relative to general equities. Nevertheless, the full impact of COVID-19 on property has yet to become clear.

Sharing the pain

The exceptional measures taken to contain COVID-19 are having a major effect on economic activity. However, unlike past major market events, Australia appears to have an overwhelming unity of support between governments, central banks and business to do whatever it takes to minimise the economic impact.

With specific relevance to property, while the economic cost to business will be severe, these costs will be felt by both tenants and landlords alike. On 7 April 2020, the government introduced a mandatory code of conduct to outline leasing principles between tenants and landlords. The objective is to share, in a proportionate manner, the financial impact of COVID-19, whilst seeking to balance the interests of tenants and landlords.

These temporary measures essentially state that landlords must not terminate a tenant’s lease for non-payment of rent and in turn, tenants must honour their lease agreements. The code also introduced guidelines for rental waivers and deferrals (to be negotiated on a case by case basis) based on the reduction of the tenant’s trade. If they can't agree, the remedy is binding mediation.

At face value this suggests that REITs are facing tough times ahead. Does this mean however that property is down and out?

Think about the cashflow waterfall

As real assets, property has physical value tied to the land it occupies and linked to the ability to generate growing income over time. While a reduction in earnings for REITs is likely, the outlook for general equities is even more uncertain.

The claims on a business’s cashflow and the order in which it becomes a receivable to others is also important. For commercial real estate, leases are a legal obligation on a tenant’s business to pay rent ahead of any other payments to equity holders. This ‘prioritisation’ means that cashflows that fuel REITs distributions will be receivable by the REIT before becoming available for dividends in general equities. This is therefore an important consideration favouring retaining REIT exposure.

Beware the timing trap

While the near-term outlook for REITs is one of uncertainty, the same goes for all asset classes. The lure of a wholesale rotation out of an asset class can be strong. However, persistence of return among asset classes is highly fickle. Predicting the path of return between asset classes is notoriously difficult to judge accurately. Switching asset allocation introduces the risk of mis-timing sudden market moves.

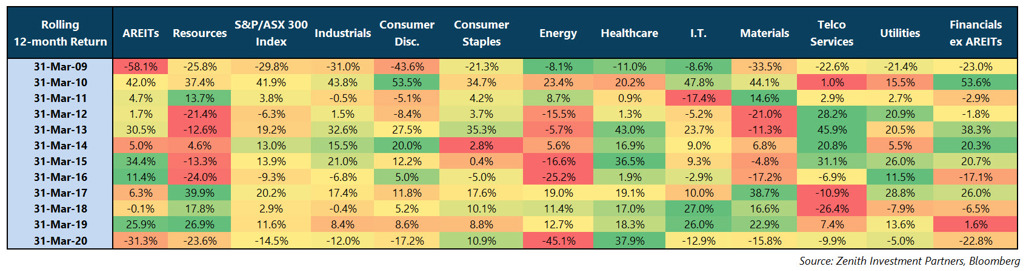

What goes for the major asset classes also holds for inter-asset class sectors. As an example, the following table shows the annual performance of each of the GICS sectors that make up the S&P/ASX 300 Index since the trough of the equities market in the GFC.

As can be seen, different sectors clearly moved at different speeds as the recovery phase kicked in. It is logical to expect that this time will be no different. Maintaining exposure to the different return drivers of an economy is just as important as a diversified portfolio of asset classes.

The search for income continues…

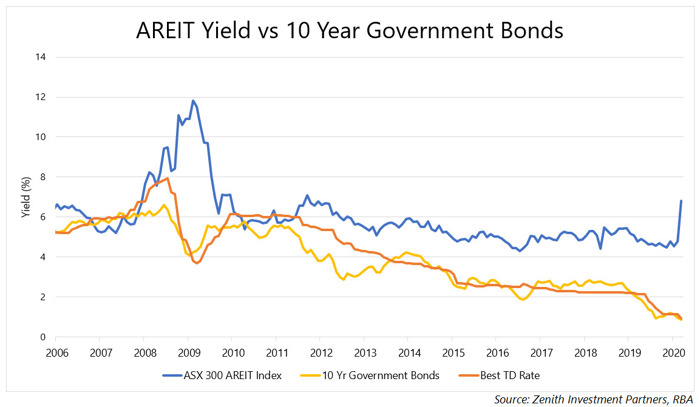

Given REITs have a strong income focus, in a world where the ‘lower for longer’ interest rates scenario has extended out to hitherto unforeseen levels, the merit of real estate remains intact. Post this crisis, we believe the demand for income generating assets will continue, if not actually increase.

...with AREITs playing a major role

Income yields from REITs relative to general equities have historically been compelling. Although the short-term outlook for earnings is challenged, as discussed previously, this applies equally to REITs and equities.

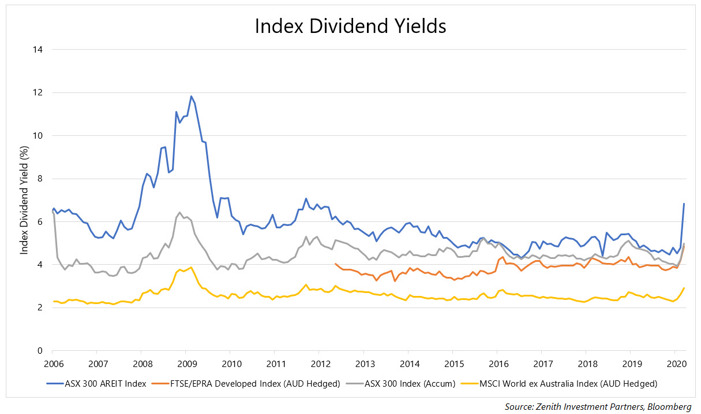

The concentration across sectors and stocks within the AREIT Index has always been a challenge to be navigated. It is noticeable however that AREITs have consistently yielded higher than GREITs. When combined with AREITs ability to generate tax advantaged income, this makes a compelling argument to retain at least some exposure to AREITs as part of a portfolio’s overall allocation to property.

Property matters

Despite the challenges COVID-19 is throwing at the real estate sector in the near term, businesses still require real estate as an operating platform as part of the value chain. It is too early to tell to what extent secular changes (which were already underway) will be fast tracked by these events. The rise of online retail, the increasing importance of logistics centres and greater demand for flexibility in office utilisation are all themes being accelerated by current events. Landlords are acutely aware of these changes and for the most part are pivoting to meet them. While there are undoubtedly some who will lose out, others stand to gain.

It is difficult to predict the extent and duration of the current viral outbreak. The key to robust portfolio management should be not to predict events, but to prepare for the unexpected. With the medium-term future for the global economy unclear, owning assets with an array of risk drivers, including REITs, should be advantageous.