In investing, the speed at which new themes capture the market's interest is only eclipsed by the speed at which that enthusiasm can turn. For sustainable investing, the move from hot to not has been brutal. We think it’s important to ask a few simple questions. Are funds abandoning sustainability? Did they overreach their aims? And will this segment recover?

Riding the cycle

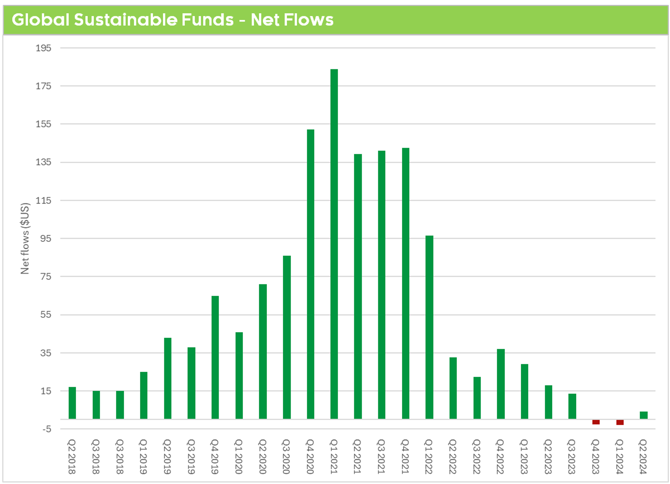

For funds focused on sustainability, quarterly flow data shows a rollercoaster of the highs and lows. While regional results are varied with Europe still bringing in solid inflows, the US funds continue to hemorrhage money. It’s fair to say the overall picture looks gloomy.

But where are these headwinds coming from? Firstly, it depends on your market. For example, in the US, ‘ESG’ is now so controversial that many funds have stopped talking about it. Politically, a Trump administration could reverse several existing frameworks and policies for the energy transition and climate. Logically, a threat to the velocity of the energy transition has caused some managers to review their investments and strategies. Regional economic uncertainties also play a role, with many renewable energy projects facing rising development costs, leaving many projects unprofitable.

While challenges in the US are notable, other jurisdictions are being more circumspect. In Europe for example, the distinction between ESG and sustainability is clearer, leading to continued substantial inflows into sustainability strategies. Regional attitudes play a huge part.

Secondly, investment styles and implementation play a part. Rotation between value and growth in equities, for example, has brought challenges to many funds, particularly where many lower carbon strategies tended to be growth-orientated. The active/passive debate has also played a part, adding further noise to viability issues for some active managers. But passive solutions can face their own headwinds, particularly around engagement actions and screening. How firms act is heavily framed by not just location, but by their investment model too.

Thirdly, many aspects of the responsible investment landscape remain unclear. Markets (and managers) hate uncertainty. Challenges like evolving disclosure frameworks, greenwash regulations and geopolitical issues make attaining sufficient clarity difficult. Many firms are hesitant to take a strong stance on products until they understand what a ‘new normal’ looks like.

Did funds overreach?

In market booms, the race to get products to market invariably means that enthusiasm can get in the way of pragmatism. The proliferation of funds pursuing ESG or sustainability between 2018 – 2021 was logical when it was believed by many that they were the solution to both a greener future and higher returns. Now regulations are getting tougher and managers are realising that the journey is more complicated than they thought, and many hurriedly created solutions have turned out not to be fit for purpose.

Market evolution works both ways. Many funds are either getting relabelled, restructured or removed altogether. This makes sense as product proliferation often outpaces intelligent design and momentum tends to swing too far ahead and too far behind before reaching a steadier state.

In the race for managers to launch products and investors to get exposure, it’s inevitable that attention on return outcomes can waver, particularly when markets are running hot. During that time, many sustainable funds generated higher returns than their more traditional peers, particularly in equities. Often, this performance was underpinned by a bias to growth stocks, often in technology. Subsequently, many of these funds suffered a cyclical downturn as markets rotated.

Is there light at the end of the tunnel for sustainable funds?

We believe the answer is yes. While some funds are finding it tougher than others, many are viewing this as business as usual, recognising that critical societal issues remain a challenge to people and portfolios alike. We think there are several key indicators to monitor.

Performance is cyclical

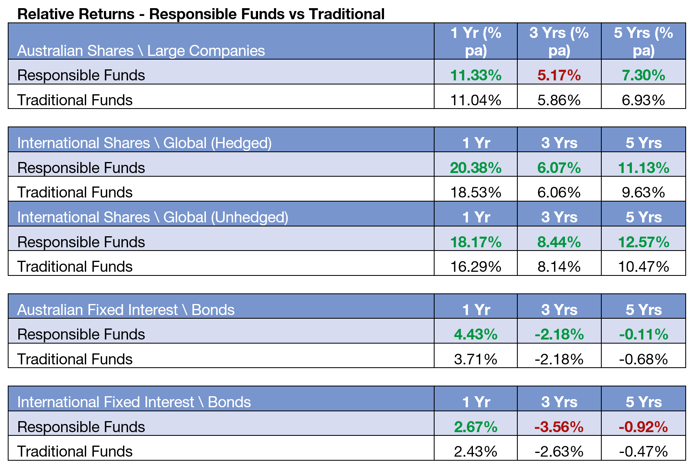

While many sustainability orientated funds underperformed their traditional peers between 2021-2023, this appears to be changing again. The following data is drawn from Zenith’s June 2024 Responsible Returns report, which measures net fund performance based on each peer group’s median return for each period.

We believe the data shows that investors don’t necessarily have to give up performance when considering sustainability issues. However, while this tends to be the longer-term trend, outcomes in the short term can be very different. We’d like to think that as data on return outcomes becomes clearer, this will support the case for sustainability investment again.

Sentiment might wane, but reporting requirements are getting stronger

Sentiment is cyclical